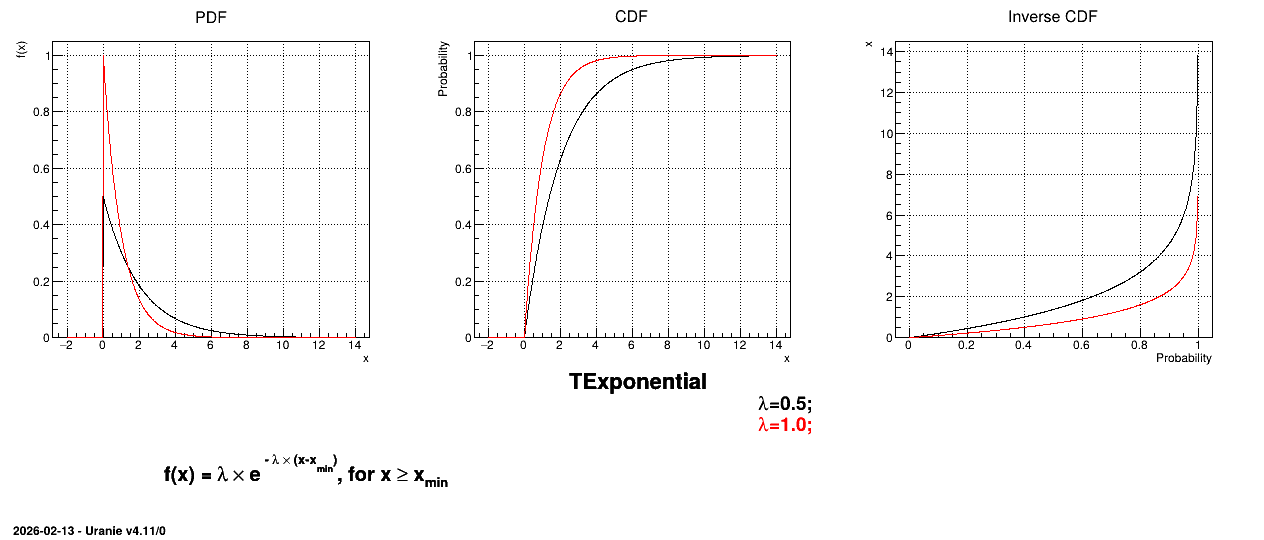

2.1.1.9. Exponential law

This law describes an exponential with a rate parameter \(\lambda\) and a minimum \(x_{\rm min}\), as

\[f(x) = \lambda \times e^{- \lambda \times (x-x_{\rm min})} \;

{\rm 1\kern-0.28emI}_{[x_{\rm min},+\infty[}(x)\]

The rate parameter \(\lambda\) should be positive.

The mean value of the exponential law can then be computed as \(\mu = \lambda^{-1}+x_{\rm min}\) while its variance can be written as \(\sigma^{2} = \lambda^{-2}\). The mode is the chosen minimum value.

Figure 2.10 shows the PDF, CDF and inverse CDF generated for different sets of parameters.

Figure 2.10 Example of PDF, CDF and inverse CDF for Exponential distributions.