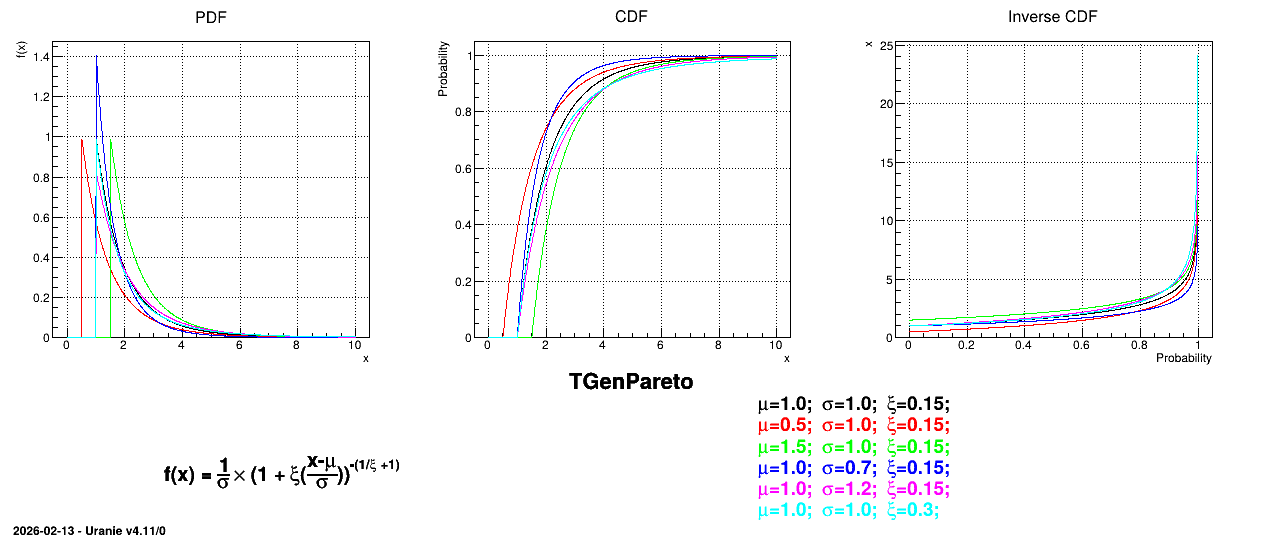

2.1.1.14. GenPareto law

This law describes a generalised Pareto distribution depending on the location \(\mu\), the scale \(\sigma\) and a shape \(\xi\), as

\[f(x) = \frac{1}{\sigma}\times \left(1 + \xi\left(\frac{x-\mu}{\sigma}\right)\right)^{-(1/\xi +1)}\]

In this formula, \(\sigma\) should be greater than 0.

The resulting mean for this distribution can be estimated as \(\mu + \sigma / (1-\xi)\) (for \(\xi < 1\)) while its variance can be computed as \(\dfrac{\sigma^{2}}{(1-\xi)^{2}(1-2\xi)}\) (for \(\xi < 0.5\)).

Figure 2.15 shows the PDF, CDF and inverse CDF generated for different sets of parameters.

Figure 2.15 Example of PDF, CDF and inverse CDF for GenPareto distributions.