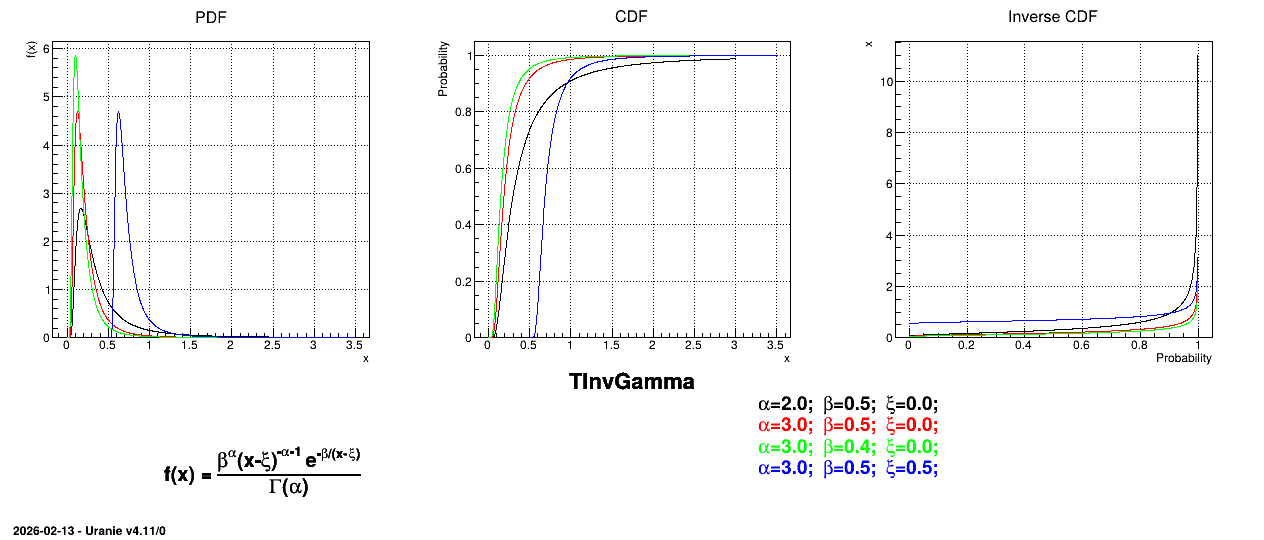

2.1.1.16. InvGamma law

The inverse-Gamma distribution is a two-parameter family of continuous probability distributions. It depends on a shape parameter \(\alpha\) and a scale parameter \(\beta\). The function is usually defined for \(x\) greater than 0, but the distribution can be shifted thanks to the third parameter called location (\(\xi\)) which should be positive.

The mean value of the Inverse-Gamma law can then be computed as \(\mu = \beta/(\alpha-1) + \xi\) (for \(\alpha > 1\)) while its variance can be written as \(\sigma^2=\dfrac{\beta^2}{(\alpha-1)^{2} (\alpha-2)}\) (for \(\alpha > 2\)).

Figure 2.17 shows the PDF, CDF and inverse CDF generated for different sets of parameters.

Figure 2.17 Example of PDF, CDF and inverse CDF for InvGamma distributions.