2.1.1.6. LogNormal law

If a random variable \(x\) follows a LogNormal distribution, the random variable \(\ln(x)\) follows a Normal distribution (whose parameters are \(\mu\) and \(\sigma\)), so

In Uranie, it is parametrised by default using \(M\), the mean of the distribution, \(E_{f}\), the Error factor that represents the ration of the 95% quantile and the median (\(E_{f} = q_{0.95} / q_{0.50}\)) and the minimum \(x_{\rm min}\). One can go from one parametrisation to the other following those simple relations

The variance of the distribution can be estimated as \({\rm Var}=(e^{\sigma^2}-1)e^{2\mu+\sigma^2} = (e^{(\frac{\ln{(E_{f})}}{1.645})^2}-1)\times (M-x_{\rm min})^{2}\) while its mean is \(e^{\mu + \sigma^2/2}\) and its mode is \(e^{\mu - \sigma^2}\).

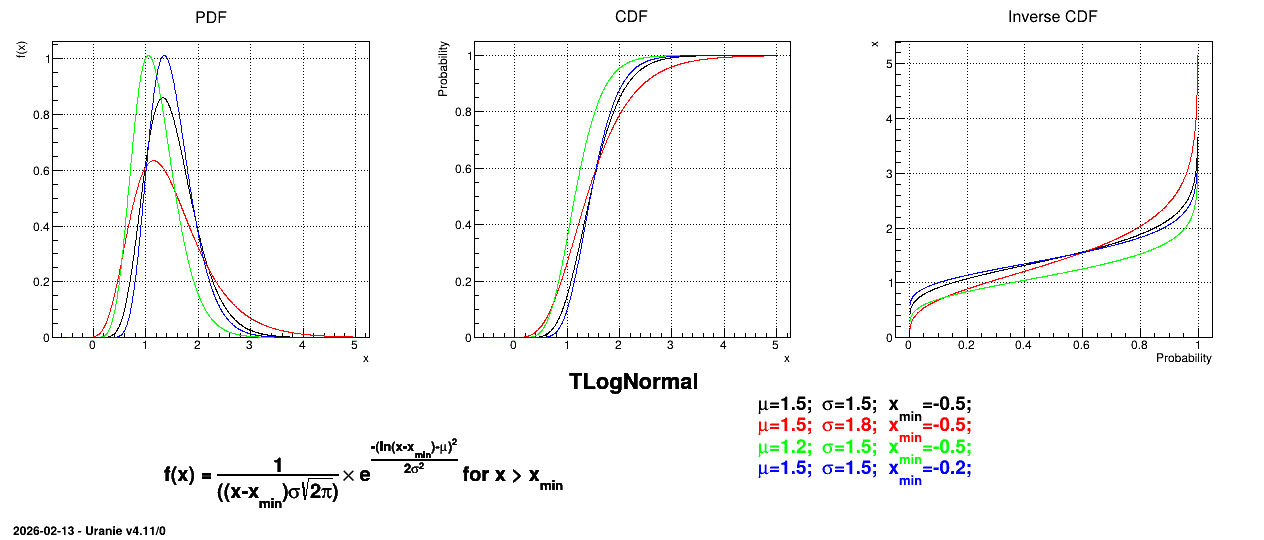

Figure 2.7 shows the PDF, CDF and inverse CDF generated for different sets of parameters.

Figure 2.7 Example of PDF, CDF and inverse CDF for LogNormal distributions.